One of the most common questions in finance is simple:

What is a good working capital ratio?

At first glance, the answer seems straightforward.

Many sources will tell you that a ratio between 1.2 and 2.0 is “healthy.”

But in practice, things are not that simple.

The Illusion of a “Good” Number

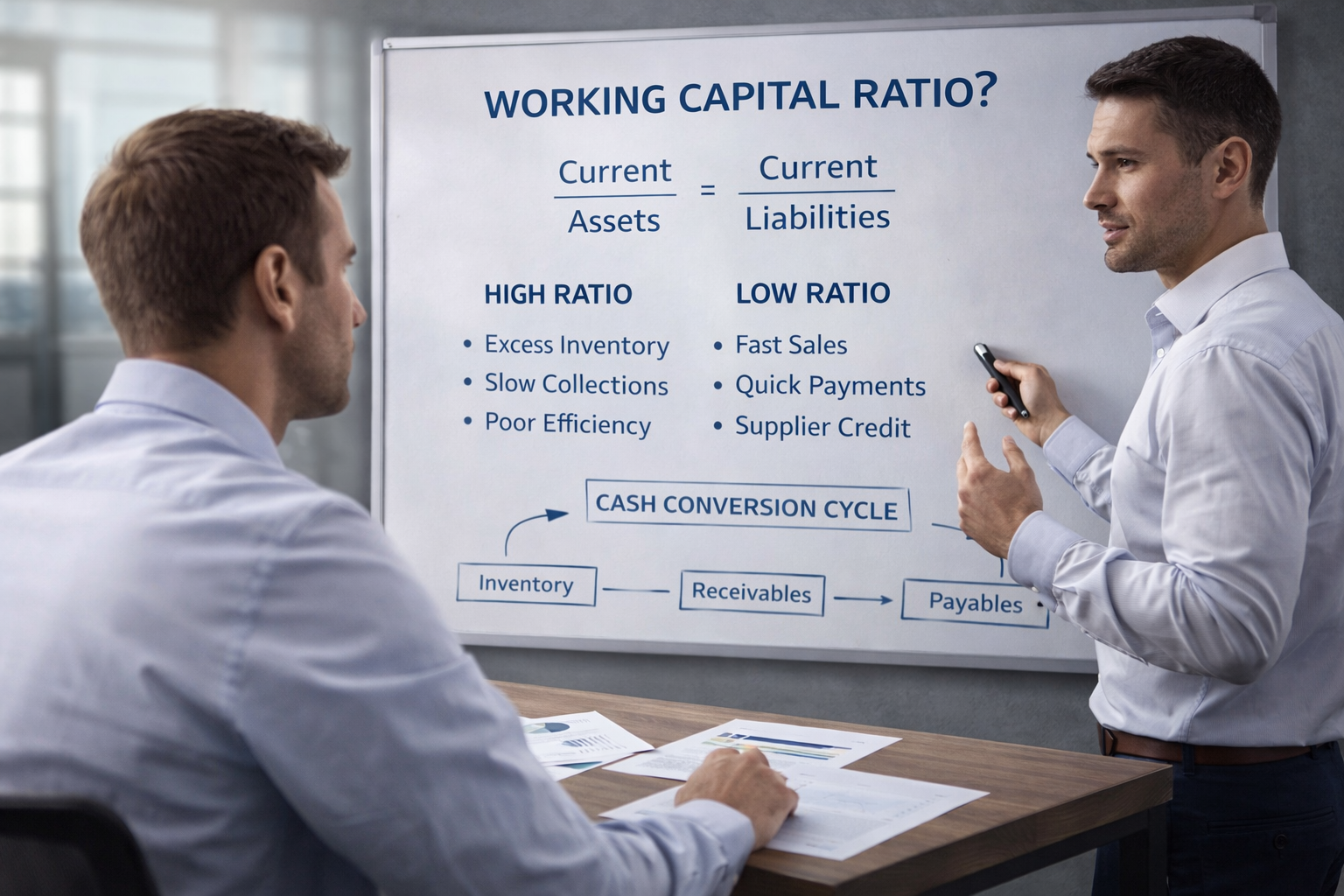

The working capital ratio is calculated as:

Current Assets ÷ Current Liabilities

It measures a company’s ability to meet its short-term obligations.

A higher ratio suggests more liquidity.

A lower ratio suggests more pressure.

But numbers, on their own, don’t tell the full story.

When a High Ratio Is Not a Good Sign

A company with a very high working capital ratio may seem financially strong.

But that is not always the case.

It could mean:

- excess inventory that is not moving

- receivables that are taking too long to collect

- inefficient use of resources

In other words, cash is trapped.

And trapped cash is not productive.

When a Low Ratio Is Not a Problem

On the other hand, some businesses operate successfully with low working capital ratios.

Retail companies, for example, often:

- sell quickly

- collect cash immediately

- pay suppliers later

This creates a short—or even negative—cash conversion cycle.

And that can be a sign of efficiency, not weakness.

The Real Question Behind the Ratio

Instead of asking:

Is my ratio good?

A better question is:

What is driving this number?

Because the ratio is just the result of deeper dynamics:

- how fast inventory moves

- how quickly customers pay

- how suppliers are managed

These are the same elements that define your cash conversion cycle.

Context Matters More Than Benchmarks

Comparing your ratio to a generic “ideal” can be misleading.

A manufacturing company and a trading business will have very different needs.

What matters is:

- your industry

- your business model

- your growth stage

Without context, the number loses meaning.

A More Practical Way to Evaluate It

To truly understand your working capital position, look beyond the ratio.

Ask:

- Is my cash cycle improving or deteriorating?

- Am I financing my operations unnecessarily?

- Is growth creating pressure or efficiency?

These questions reveal more than any single metric.

The Link With Cash Flow and Forecasting

Your working capital ratio is not static.

It evolves.

And it directly impacts your ability to forecast cash flow.

If your ratio reflects inefficiencies:

- your forecasts will show gaps

- your dependence on financing will increase

If it reflects control:

- your forecasts become more predictable

- your decisions become more strategic

Final Reflection

A good working capital ratio is not a number.

It is a reflection of how your business operates.

Some companies look strong on paper but struggle in reality.

Others appear tight—but operate with precision and control.

The difference is not the ratio itself.

It is the understanding behind it.

Because in the end, financial strength is not about hitting a target number. It is about knowing what that number really means.